》View SMM Metal Quotes, Data, and Market Analysis

》Subscribe to View Historical Spot Price Trends of SMM Metals

At the beginning of December, the US Beige Book showed optimism about economic growth but also expressed concerns over Trump's tariff policies. The US November YoY non-seasonally adjusted CPI recorded 2.7%, up from the previous value of 2.6%, indicating that US inflation had not effectively continued to decline. The US dollar rose sharply, approaching the 107 level. In the Chinese market, the Central Politburo meeting signaled policies for stabilizing growth and expanding domestic demand next year, emphasizing relatively loose liquidity and counter-cyclical adjustments to stimulate the market, boosting confidence in the domestic macro market. Copper prices approached a high of 76,000 yuan/mt. However, with the US Fed's December 25bp interest rate cut and a reduction in the 2025 rate cut space, the US dollar surged to 108, putting significant pressure on copper prices, which consecutively dropped to around 74,000 yuan/mt.

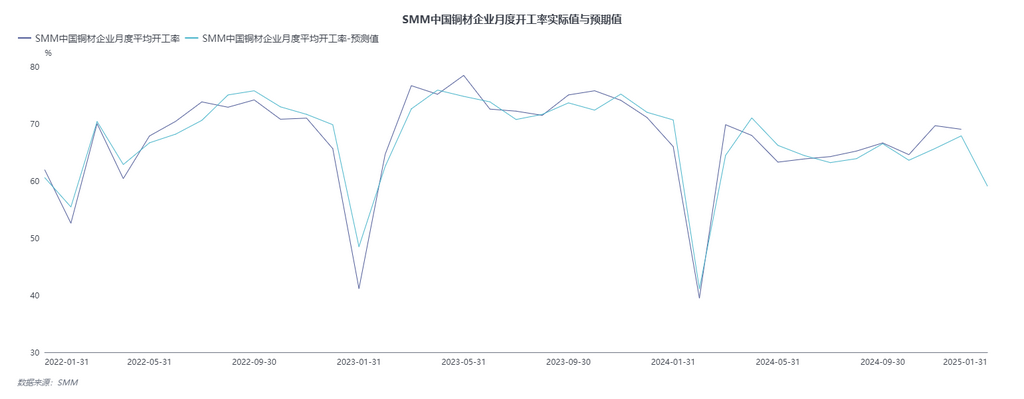

On the fundamentals, with the finalization of long-term contract prices for imported copper concentrates, long-term contract quotes for domestic and foreign trade copper cathode were successively released, but transactions were less than satisfactory. Copper cathode production in December increased by 90,400 mt MoM, a rise of 8.99%. The operating rate of copper semis in December decreased as expected by 2.06 percentage points MoM, while the destocking of copper cathode in the social market slowed to 66,400 mt. According to SMM and market exchanges, rumors in mid-to-late December suggested that "reverse invoicing" would be implemented starting January 1, 2025, potentially increasing procurement costs for secondary copper rod plants. Some enterprises planned to temporarily halt production in early January to observe the market, and the operating rate of secondary copper rods was also below expectations.

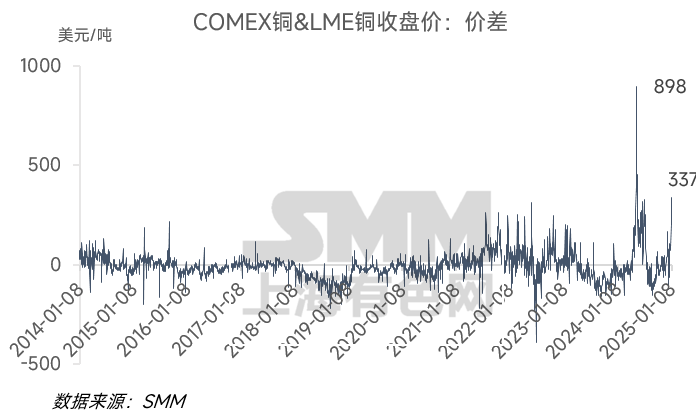

Looking ahead to January, on the first trading day of 2025, copper prices fell below 73,000 yuan/mt due to the strong rise of the US dollar to the 109 level. However, low prices attracted downstream pricing, and copper prices quickly rebounded above 73,000 yuan/mt, indicating that the 73,000 yuan/mt level still provided support. Subsequently, a series of "Trump" news led to short-term profit-taking in the US dollar, which briefly pulled back to above the 107 level, allowing copper prices to return above 74,000 yuan/mt. However, multiple recent moving averages continued to exert resistance, with 75,500 yuan/mt expected to gradually show resistance. Additionally, strong non-farm payrolls data once again stirred the market, pushing the US dollar above the 109 level. The COMEX and LME markets saw a resurgence of high price spreads. SHFE copper did not directly exhibit a downward trend due to the rising US dollar, but resistance above 76,000 yuan/mt became more pronounced.

At the end of January, the Chinese New Year holiday will begin. According to SMM and market exchanges, small enterprises will take an early holiday, while medium and large enterprises will mostly arrange holidays after the 20th. The operating rate of copper semis is expected to decline MoM. With the earlier opening of the SHFE/LME price ratio, January imports of copper are expected to reach 320,000 mt, and copper cathode in the social market will show an inventory buildup trend, weakening fundamental consumption support for copper prices.

》View SMM Metal Industry Chain Database